Reading the results

What every Monte Carlo output means: the five key metrics, the return and drawdown scenario cards, the simulated equity-path band chart, and the two distributions.

A finished run produces four blocks, top to bottom: Key Metrics, Return Scenarios, Drawdown Scenarios, and the charts (Portfolio Growth + Distributions). Here's how to read each.

Key Metrics

| Card | Meaning |

|---|---|

| Avg. Net Profit | Average ending value minus initial capital, across all simulations. |

| CAGR | Compound annual growth rate of the average ending value. |

| Expected DD | The average maximum drawdown across all simulations, in % and $. Note this is the expected (typical) worst valley — half your simulated futures were worse than the median drawdown. |

| MAR Ratio | CAGR ÷ expected drawdown, the risk-adjusted one-number summary of the simulated distribution. |

| Prob. of Profit | The share of simulations ending above starting capital. The app caps the display at ">99%" — and its own help text is worth internalizing: paths are resampled from the backtest window, so they can't contain conditions that window never saw. This is not a forecast. |

Return Scenarios (CAGR)

Five cards slice the distribution of terminal values: Absolute Best, Best Case (95%), Most Likely (50%), Worst Case (5%), Absolute Worst — each as an annualized growth rate with the terminal dollar value. The 5%/95% cards are the useful pair: a 90% band of outcomes. The absolutes are single most-extreme paths — anecdotes, not planning numbers.

Drawdown Scenarios

The same slicing applied to each path's maximum drawdown: Absolute Best DD (mildest ever), Best Case DD (5%), Typical DD (50%) (median), Worst Case DD (95%), Absolute Worst DD (deepest ever).

This row is the reason to run the simulation at all. The question to answer honestly: could I keep trading the system through the Worst Case DD (95%) number? If not, the construction is oversized for you — go back to the Builder and scale down before the market runs the experiment for you.

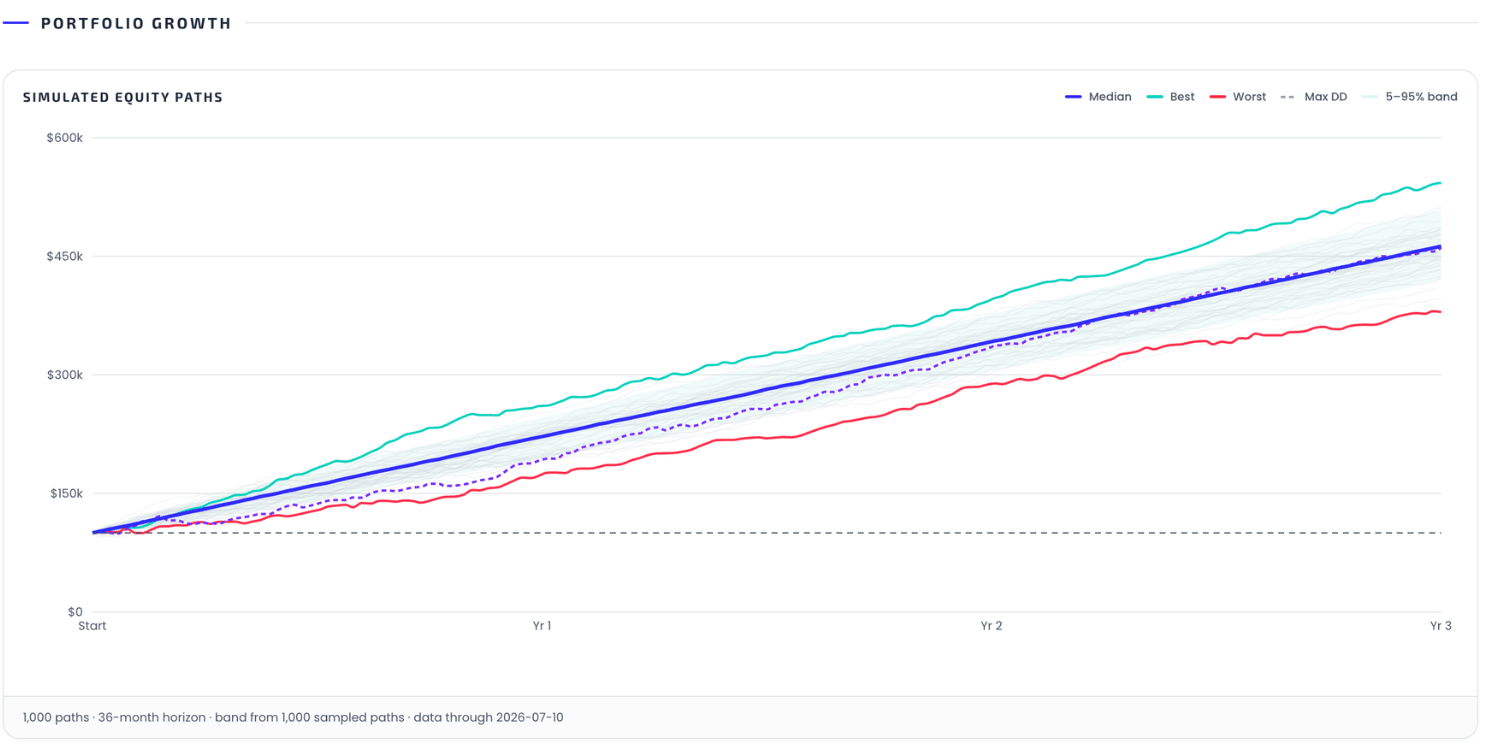

Portfolio Growth — simulated equity paths

The band chart compresses every path into one picture:

- Median line — the 50th percentile at each point in time.

- 5–95% band — where 90% of paths lived at each step.

- Best / Worst lines — the single best and worst terminal paths.

- Max DD line (dashed) — the path containing the deepest drawdown, which is usually not the worst terminal path: a path can end fine and still have been horrible to live through.

- The faint lines are individual sampled paths; the dashed horizontal line is your starting capital.

The footer states the run's facts: paths, horizon, injected events, and the data-through date.

Distributions

Two histograms with 5th/50th/95th percentile markers:

- Return distribution — cumulative return over the horizon across paths.

- Drawdown distribution — each path's max drawdown. Typically right-skewed: a long tail of rare-but-deep valleys. The tail is the part worth staring at.