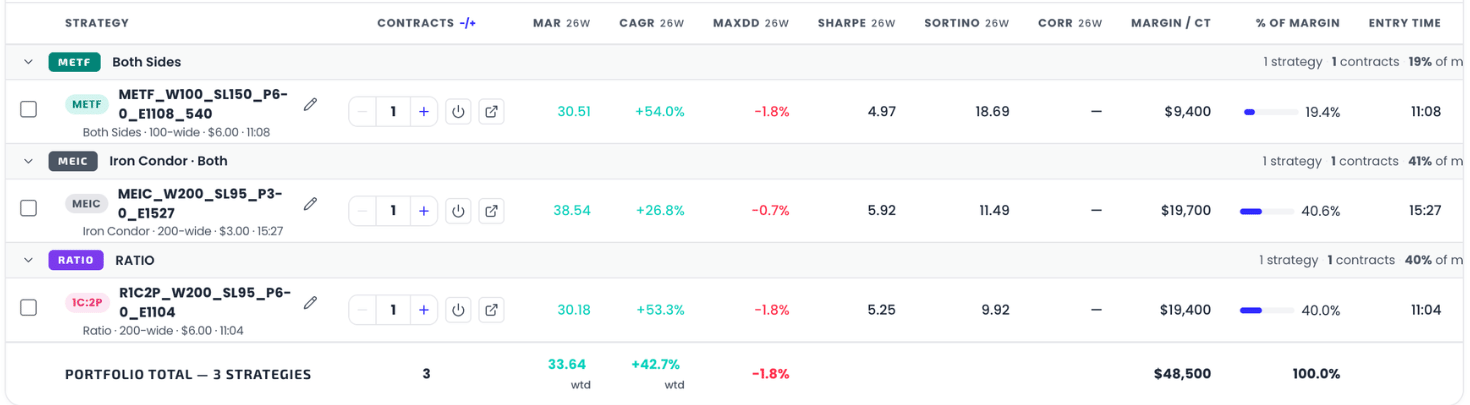

The composition table

Every column and control of the Selected Strategies table: contract steppers, enable/disable, aliases, correlation flags, family groups and the portfolio-total footer.

The composition table is where you shape the portfolio: how many contracts of each strategy, which stay enabled, and which are pulling their weight.

The toolbar

- Filter strategies… — case-insensitive text filter over names and ids.

- Correlated > (slider) — the correlation threshold (adjustable 0.40–0.95). Strategies whose daily returns correlate with another pick above this value get flagged in the table. Higher = stricter.

- Correlated only (n) — narrows the table to just the flagged rows so you can review them and decide what to drop. Nothing is removed automatically.

- Columns — show, hide and drag-reorder columns; the layout is remembered per device. Performance columns carry a badge with the active period.

The columns

| Column | Meaning |

|---|---|

| Strategy | Family badge, name (or your alias), and the parameter summary underneath. |

| Contracts −/+ | Per-strategy sizing: the steppers scale this strategy's allocation (1–999). |

| MAR | This strategy on its own: CAGR ÷ Max Drawdown, on the standardized $100k account, over the active period. |

| CAGR | Compound annual growth of the strategy on its own, standardized. |

| MaxDD | The strategy's own worst peak-to-trough decline, as % of the standardized account. |

| Sharpe / Sortino | Risk-adjusted return per unit of total / downside volatility. |

| Corr | The strategy's highest correlation with any other enabled pick — values above the threshold render in coral with a badge listing the partners. |

| Margin / ct | Margin per contract: (width − premium) × 100 — the spread's max loss. |

| % of margin | This row's share of the portfolio's total deployed margin, drawn as a bar. |

| Entry Time | The strategy's entry time (via Columns you can also show Width, Stop Loss, Premium and EMA Variant as separate columns). |

Per-strategy ratio metrics (MAR, CAGR, MaxDD, Sharpe, Sortino) are contract-invariant: they describe the strategy, not your sizing. What scales with your contract counts: total margin, total P/L, and margin share.

Row controls

- −/+ steppers — size the allocation.

- Power toggle — disable a strategy without deleting it: the row gets an OFF badge, is excluded from every aggregate, and keeps its place for later re-enabling. Useful for A/B-ing a construction.

- Pencil — give the strategy your own alias (prefix, suffix, comment).

- ✕ — remove the row entirely.

- LOW MAR badge — appears when a strategy's own MAR drops below 1.0 over the active period; a prompt to reconsider, not a verdict.

Family groups and the footer

Rows group by strategy family (METF, Put-only, Call-only, Iron Condor, Ratio, Imported), each group collapsible, with contracts and margin share summarized per family.

The sticky Portfolio total footer shows: total contracts, the margin-weighted average MAR and CAGR (marked wtd), the worst per-strategy drawdown, total netted margin, and 100% margin share. Note the wtd numbers are weighted averages of the parts — the compounded portfolio numbers, which stack gains across strategies, live in Portfolio Metrics and are typically different.