A settlement method in which an expiring in-the-money option pays the difference between the settlement value and the strike in cash — (settlement value − strike) × $100 for calls, (strike − settlement value) × $100 for puts — instead of delivering the underlying. All SPX and SPXW options are cash-settled.

Cash settlement is one of the three structural properties that separate SPX index options from equity options like SPY — the other two are European-style exercise and Section 1256 tax treatment.

How does SPX settlement work?

At expiration, every SPX option is measured against one official settlement value of the S&P 500 index. If the option is in the money against that value, it is exercised automatically and settles to cash at intrinsic value. If it is out of the money, it expires with no value and no further obligation. Which settlement value applies — Friday's opening print or expiration day's close — depends on whether the contract is AM- or PM-settled.

Two mechanics do all the work. First, automatic exercise: expiring index options that finish in the money by as little as $0.01 are exercised by the OCC without anyone lifting a finger — there is no "letting it expire" as a separate choice once the settlement value is fixed. Second, the settlement value itself: a single official number, published by the exchange, that every expiring contract in that series settles against. Not the last price on your chart — the official print.

That second point is where most surprises live, and it is the reason the AM/PM distinction matters more than it first appears.

Are SPX options cash settled?

Yes. Every SPX and SPXW option is cash settled: an in-the-money contract resolves to a cash amount — intrinsic value × $100 — and an out-of-the-money contract expires with no value. There is no delivery of shares, no stock position on Monday morning, and no pin risk.

The arithmetic is one line. Suppose the settlement value comes in at 6,312:

| Position at expiry | Settlement math | Cash flow |

|---|---|---|

| Long 6,300 call | (6,312 − 6,300) × $100 | +$1,200 credit |

| Short 6,300 call | (6,312 − 6,300) × $100 | −$1,200 debit |

| Long 6,320 call | out of the money | $0 — expires with no value |

| Short 6,350 put | out of the money | $0 — obligation ends |

Compare that with SPY, an American-style equity option with physical delivery: a short SPY call that expires in the money delivers 100 short shares per contract into the account, complete with weekend gap exposure and a Monday-morning cleanup trade. Cash settlement removes that entire category of aftermath — including pin risk, the classic expiration problem of not knowing whether a short option that closed at-the-money will be assigned shares or not. With SPX there is nothing to assign: the settlement value either puts the contract in the money or it doesn't, and the result is cash either way.

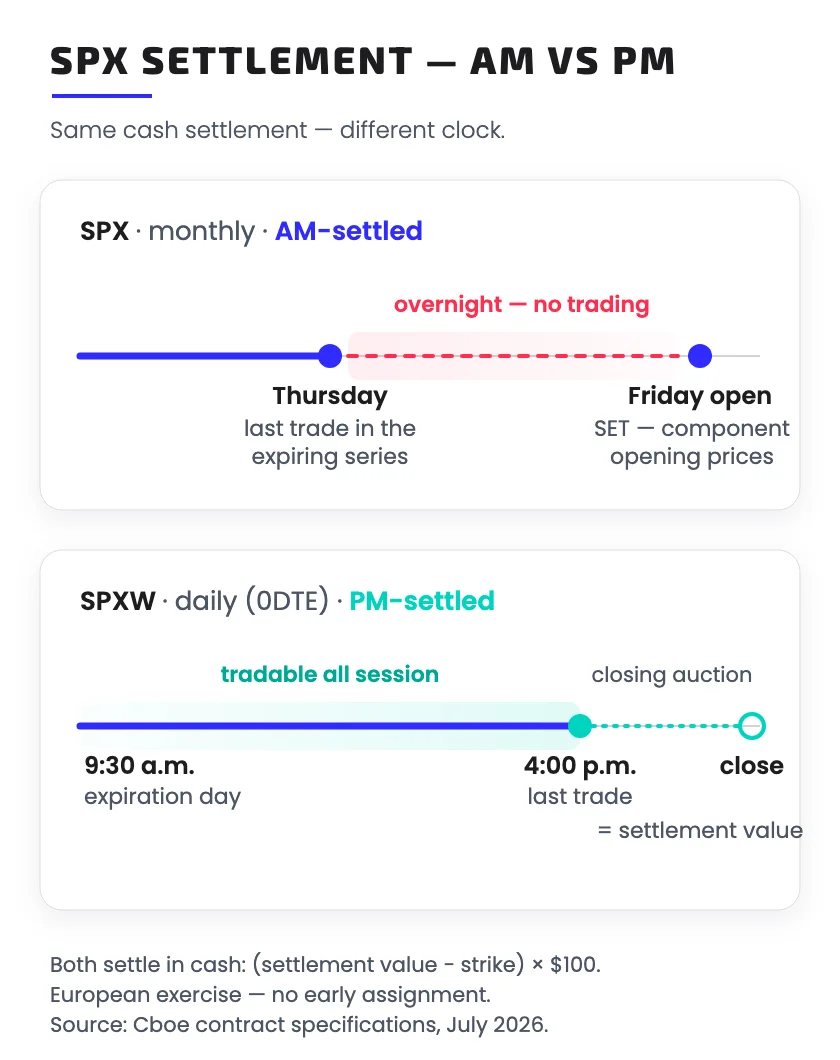

AM vs PM settlement: which SPX options settle when?

Standard SPX monthlies (third Friday) are AM-settled: they stop trading Thursday afternoon and settle against SET, a value computed from Friday's opening prices of all 500 component stocks. Everything else — SPXW weeklys and dailies, end-of-month series — is PM-settled against the index close on expiration day.

| SPX (standard monthly) | SPXW (weekly / daily) | |

|---|---|---|

| Expiration | Third Friday of the month | Every trading day, Mon–Fri |

| Settlement | AM — Friday opening | PM — expiration day close |

| Settlement value | SET, from each component's opening price | Official S&P 500 closing value |

| Last trade in expiring series | Thursday session before settlement | 4:00 p.m. ET on expiration day |

| Time between last trade and settlement | An overnight session you cannot trade against | Minutes (closing auction) |

The AM mechanism deserves the extra sentence, because it is genuinely odd the first time you meet it. SET is not the index level at 9:30. It is computed from the opening auction price of each of the 500 component stocks — and components open at slightly different times. On a calm morning SET lands near the visible index open; on a gap morning it can land meaningfully away from both Thursday's close and the 9:30 index print, and the final value is published mid-morning after the last component opens. A position held into AM settlement is therefore exposed to an overnight move plus an opening rotation, with no ability to react — the contract stopped trading the afternoon before.

PM settlement removes the gap: the expiring SPXW contract trades until 4:00 p.m. ET and settles against the official close of the same session. The residual nuance is the closing auction itself — more on that in the in-the-money section below.

SPXW vs SPX: what's the difference?

SPX and SPXW are the same underlying, the same $100 multiplier, the same European-style cash settlement — the difference is the expiration calendar and the settlement time. SPX is the AM-settled third-Friday monthly; SPXW is the PM-settled series with an expiration every single trading day.

SPXW began as Friday-only weeklys, added Monday and Wednesday expirations, and completed the set in 2022 when Cboe listed Tuesday (April 2022) and Thursday (May 2022) expirations. Since then there has been an SPXW expiration every trading day — which is precisely what made daily 0DTE trading a category rather than a Friday event. When traders say "SPX 0DTE", the contracts are almost always SPXW series: on four days out of five they are the only same-day expiration available, and even on third Fridays the AM-settled monthly stopped trading the afternoon before, so the tradable 0DTE contract that Friday is again the PM-settled SPXW.

Both roots share Section 1256 tax treatment (the 60/40 rule) and both are exercised only at expiration. For strategy purposes the practical distinction reduces to one question: do you want your position measured against tomorrow's opening rotation (SPX monthly), or against a close you can watch — and trade against — until 4:00 p.m. (SPXW)? Our own automation only ever touches PM-settled SPXW series; every mechanic in the rest of this article is the PM case unless labeled otherwise.

Can SPX options be assigned early?

No. SPX and SPXW are European-style options: exercise can only happen at expiration, so early assignment is structurally impossible. A short SPX option cannot be assigned on a random Tuesday — the position's obligations are fixed until the settlement value exists.

"European style" describes exercise timing, not geography — these are US contracts on a US exchange. Two consequences follow, and both matter operationally:

- The structure stays intact. In a defined-risk position — a credit spread, an iron condor — no leg can be pulled out early by a counterparty. An American-style short leg can be assigned before expiration (SPY shorts around ex-dividend dates are the classic case), leaving the "defined-risk" structure temporarily broken into a stock position plus a leftover long option. On SPX that failure mode does not exist: the maximum loss computed at entry stays the maximum loss.

- European ≠ locked in. Exercise is restricted to expiration; trading is not. An SPX position can be opened and closed any time the market is open, including seconds before the 4:00 p.m. cutoff on expiration day. The restriction only removes the counterparty's ability to exercise against you early.

For an automated system this is the difference between modeling one deterministic event (settlement at a known time against an official value) and modeling a random one (assignment that can arrive any day the position is in the money). It is a large part of why SPX became the default underlying for systematic 0DTE strategies.

What time do 0DTE options stop trading and expire?

An expiring SPXW contract trades until 4:00 p.m. ET on its expiration day (1:00 p.m. on half-day holidays) and settles against that session's official close. Non-expiring SPX and SPXW series trade longer — until 4:15 p.m. in the regular session, plus overnight Global Trading Hours.

SPX options trading hours, as listed by Cboe (July 2026, all times ET):

| Session | Hours (ET) | Notes |

|---|---|---|

| Global Trading Hours (overnight) | 8:15 p.m. – 9:25 a.m. | Sunday night through Friday morning, 24×5 access |

| Regular session | 9:30 a.m. – 4:15 p.m. | Non-expiring series trade the full window |

| Curb session | 4:15 p.m. – 5:00 p.m. | Post-close session |

| Expiring SPXW, on expiration day | trades until 4:00 p.m. | 1:00 p.m. on half-day holidays |

| Expiring SPX monthly | last trade: Thursday session before third-Friday AM settlement | AM-settled against Friday's SET |

Three details trip people up. First, the 15-minute tail: between 4:00 and 4:15 p.m., non-expiring SPX options keep trading while the cash index has stopped updating — pricing in that window keys off futures, and the expiring contract is already gone. Second, broker cutoffs: the exchange session and your broker's order-entry window are not the same thing; many brokers restrict or cut off orders in expiring contracts before 4:00, and overnight-session access varies by broker. Third, expiration ≠ settlement: the expiring SPXW stops trading at 4:00, but the number it settles against is the official close computed from the closing auction — published minutes later, and not always identical to the last level you saw tick.

What happens if a 0DTE option expires in the money?

It is exercised automatically and settles to cash at intrinsic value against the official settlement value — not at the price it last traded, and not at zero because you stopped watching it. A short option 12 points in the money at settlement produces a $1,200-per-contract debit, posted to the account after the close.

This is the section we can write from operating experience rather than from a spec sheet: we run automated SPX 0DTE strategies live, every trading day, and settlement is where the paper mechanics become account entries.

Early in running that automation live, one of our short options went into the close about 12 points in the money. On screen, nothing happened at 4:00 — no closing fill, no alert, just a position that stopped trading. The settlement print arrived after the close, the contract settled at intrinsic value — 12 × $100, roughly $1,200 per contract, debited that evening — and the day's true result was decided by a number published while the screen was already quiet. The lesson was not that settlement is dangerous; it is that "expired" never means "went away." An expiring in-the-money short is a real liability, priced off an official value you can no longer trade against after 4:00 p.m.

The settlement print is the only price that matters at expiry. A strike that looked marginally out of the money at 3:59:59 can settle in the money once the closing auction prints, and vice versa — the official close is computed from closing auction prices, not from the last on-screen trade. Anything still open at 4:00 p.m. has accepted that print, whatever it turns out to be.

That experience hardened into two operating rules that generalize beyond our stack. First, expiry is a decision, not a default: an automated system needs explicit logic for every contract approaching the cutoff — close it before 4:00 at a known price, or hold it through settlement and accept the auction print. Silence is the second choice, whether it was intended or not. Second, reconcile against the settlement value, not the last quote: our end-of-day accounting marks every expired contract against the official settlement value, because that is what the broker will post — a backtest or P/L report that values expiring positions at the 4:00 p.m. quote instead will quietly disagree with the account statement, and on auction-moved days the disagreement is not small. Cash settlement makes SPX operationally clean — one underlying, no share deliveries, deterministic timing — but it replaces assignment risk with a subtler obligation: knowing exactly which print your position settles against, and being deliberate about still owning it when that print arrives.

Terms & Definitions

- Cash Settlement

- A settlement method in which an expiring in-the-money option pays the difference between the settlement value and the strike in cash (× the $100 multiplier) instead of delivering the underlying. All SPX and SPXW options settle in cash.

- European-Style Option

- An option that can be exercised only at expiration, never before. SPX and SPXW options are European-style, which makes early assignment structurally impossible; positions can still be traded or closed at any time during market hours.

- SPXW

- The Cboe root symbol for PM-settled S&P 500 index options with weekly and daily expirations. SPXW contracts expire every trading day and settle against the official index close — the series behind 0DTE trading.

- SET

- The exercise-settlement value for AM-settled standard SPX monthly options: calculated from the opening auction price of each S&P 500 component stock on the third Friday, and published mid-morning once all components have opened.

- Pin Risk

- The uncertainty, in physically settled options, of not knowing whether a short option that finishes at or near the money will be assigned shares after the close. Cash-settled index options like SPX eliminate pin risk — there are no shares to assign.

- 0DTE

- Zero Days to Expiration — options that expire on the day they are traded. On SPX, daily SPXW expirations make 0DTE strategies tradable every session.

Frequently Asked Questions

- Are SPX options cash settled?

- Yes — every SPX and SPXW option is cash settled. An in-the-money contract resolves to intrinsic value × $100 in cash against the official settlement value, and an out-of-the-money contract expires with no value. No shares are delivered in either direction.

- Can SPX options be assigned early?

- No. SPX and SPXW options are European-style, so exercise — and therefore assignment — can only occur at expiration. Positions remain fully tradable until their last trading time; only early exercise by a counterparty is impossible.

- What time do 0DTE options stop trading and expire?

- Expiring SPXW contracts stop trading at 4:00 p.m. ET on expiration day (1:00 p.m. on half-day holidays) and settle against that session's official close. Non-expiring SPX and SPXW series trade until 4:15 p.m., plus overnight Global Trading Hours (8:15 p.m.–9:25 a.m. ET, per Cboe as of July 2026).

- What happens if a 0DTE option expires in the money?

- It is exercised automatically and settles in cash at intrinsic value — the in-the-money amount × $100 — against the official closing settlement value, with the cash posted to the account after the close. A short contract 12 points in the money settles as a $1,200-per-contract debit; there is no share assignment on SPX.

Mandatory pit stop: Options trading involves significant risks and is not suitable for every investor. Past results are no guarantee of future performance.